Mastering personal finances can feel daunting, but effective tools can transform the process. Personal finance software offers a powerful solution, streamlining budgeting, investment tracking, and financial planning. This guide explores the diverse landscape of available software, highlighting key features, benefits, and integration capabilities, ultimately empowering you to make informed decisions about your financial future.

From simple budgeting apps to sophisticated investment trackers, the market offers a wide array of options catering to various needs and experience levels. We’ll delve into the functionalities of different software categories, compare popular choices, and address common concerns regarding data security and privacy. Understanding the broader context of financial literacy and emerging trends in this field will further equip you to navigate the world of personal finance with confidence.

Defining Personal Finance Software

Personal finance software provides individuals and families with tools to manage their financial lives more effectively. These applications range from simple budgeting tools to sophisticated investment trackers, offering a variety of features designed to improve financial literacy and decision-making. Understanding the capabilities and categories of this software is crucial for choosing the right tool to meet individual needs.Personal finance software typically includes core functionalities such as budgeting, expense tracking, income recording, and reporting.

More advanced features might include investment tracking, debt management tools, tax preparation assistance, and financial goal setting. The user interface plays a critical role in determining how easily individuals can interact with and benefit from these features.

Software Categories

Different software caters to specific financial needs. Budgeting apps focus primarily on tracking income and expenses, often providing visual representations of spending habits to help users identify areas for improvement. Investment tracking software monitors portfolio performance, providing insights into returns and risk. Tax preparation assistance software simplifies the process of filing taxes, guiding users through the necessary steps and calculations.

Other categories include retirement planning tools, debt management programs, and even software that facilitates financial goal setting and progress tracking.

User Interface and User Experience

The user interface (UI) is paramount to a positive user experience. A well-designed UI should be intuitive and easy to navigate, presenting financial data in a clear and understandable manner. For example, a good budgeting app might use charts and graphs to visually represent spending patterns, while an investment tracking application might display portfolio performance with interactive dashboards.

Poorly designed UIs, on the other hand, can lead to frustration and decreased user engagement, potentially hindering the software’s effectiveness. A cluttered interface, for instance, could make it difficult to find important information, while a lack of clear visual cues could make the software feel overwhelming and confusing. A good UI should be visually appealing, easy to understand, and efficient to use.

Comparison of Popular Personal Finance Software

The following table compares four popular personal finance software options, highlighting their key features and pricing models. This is not an exhaustive list, and the best software for a particular individual will depend on their specific needs and preferences.

| Software | Key Features | Pricing Model | Strengths |

|---|---|---|---|

| Mint | Budgeting, expense tracking, investment tracking, credit score monitoring | Free (with ads), Premium subscription available | User-friendly interface, comprehensive features, integration with multiple financial accounts. |

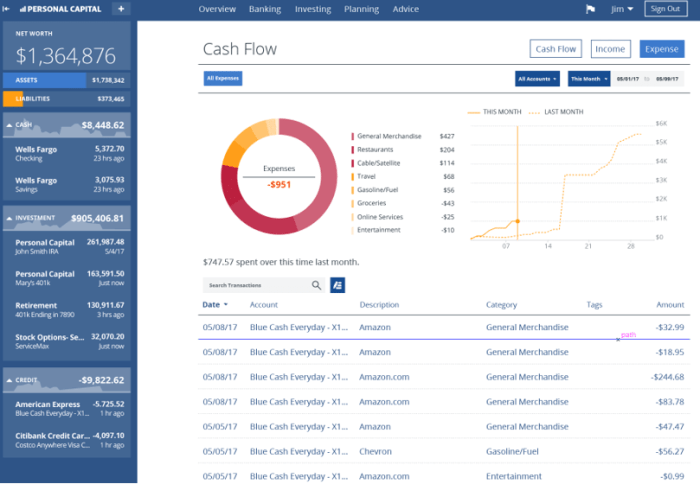

| Personal Capital | Investment tracking, retirement planning, budgeting, net worth tracking | Free (basic features), Premium subscription available | Excellent investment tracking capabilities, detailed financial planning tools. |

| YNAB (You Need A Budget) | Budgeting, goal setting, debt management | Subscription-based | Focus on mindful spending and goal-oriented budgeting. |

| Quicken | Budgeting, expense tracking, investment tracking, tax preparation assistance | One-time purchase or subscription | Comprehensive features, powerful reporting tools, long-standing reputation. |

Key Features and Benefits

Personal finance software offers a range of features designed to simplify and improve various aspects of managing personal finances. These features provide significant benefits across different life stages and financial situations, from budgeting and tracking expenses to long-term financial planning. The advantages extend beyond simple record-keeping, offering tools to enhance financial literacy and promote healthier financial habits.Effective personal finance software streamlines financial management, offering significant advantages for diverse user groups.

Automated features further enhance efficiency and provide valuable insights into spending habits, enabling users to make informed decisions about their finances. Security is also a key consideration, with reputable software providers implementing robust measures to protect sensitive financial data.

Benefits for Different Demographics

Personal finance software caters to the specific needs of various demographics. Students can use it to track expenses, create budgets, and avoid overspending while managing limited funds. Young professionals benefit from features that assist in saving for major purchases, managing debt, and planning for long-term financial goals like retirement. Families find value in tools that help manage household budgets, track shared expenses, and plan for children’s education.

Retirees can utilize the software to monitor income and expenses, manage investments, and ensure their financial security in retirement. For example, a young professional might use budgeting tools to allocate funds for rent, student loan repayments, and savings, while a family might utilize expense tracking to monitor spending across various household categories.

Advantages of Automated Features

Automated features are a cornerstone of effective personal finance software. Bill reminders eliminate the risk of missed payments and associated late fees. Automatic transaction categorization saves time and effort, providing a clear picture of spending habits. Budgeting tools, often integrated with expense tracking, allow for proactive financial planning and management. For instance, the automated categorization of transactions can quickly identify areas of overspending, prompting users to adjust their budget accordingly.

Bill reminders ensure timely payments, avoiding penalties and maintaining a positive credit score.

Security Measures in Personal Finance Software

Security is paramount when choosing personal finance software. Reputable providers employ various security measures, including data encryption, two-factor authentication, and robust password protection. Some providers also offer fraud detection and alerts, providing an additional layer of protection against unauthorized access or fraudulent activity. The level of security varies between providers, so careful research is crucial before selecting a software.

For example, some software utilizes bank-level encryption to protect sensitive data, while others may offer multi-factor authentication to verify user identity.

Potential Drawbacks and Limitations

While personal finance software offers numerous benefits, it’s important to acknowledge potential drawbacks.

- Initial setup and data entry can be time-consuming.

- Accuracy relies on diligent data input; inaccuracies can lead to flawed financial insights.

- Over-reliance on software may hinder the development of personal financial literacy.

- Some software may have limited compatibility with certain financial institutions.

- Subscription fees can represent an ongoing cost.

- Security breaches, though rare, remain a possibility.

Integration with Other Financial Tools

Seamless integration with other financial tools is a crucial aspect of effective personal finance software. This capability significantly streamlines the process of managing your finances by consolidating data from various sources into a single, unified view. The level of integration directly impacts the software’s usefulness and the overall user experience.The ability to automatically import data from bank accounts, credit cards, and investment platforms eliminates the tedious manual entry of transactions, saving users considerable time and effort.

This automation also reduces the risk of human error, ensuring the accuracy of financial data used for budgeting, analysis, and forecasting.

Data Security and Privacy Concerns in Integration

Integrating with external services presents challenges related to data security and privacy. Personal financial information is highly sensitive, and any breach could have severe consequences. Software providers must employ robust security measures, such as encryption and secure APIs, to protect user data during transmission and storage. Transparency about data handling practices and adherence to relevant privacy regulations (like GDPR and CCPA) are also essential to build user trust.

A failure to adequately address these concerns can lead to loss of user confidence and potential legal liabilities.

Comparison of Software Integration Capabilities

The following table compares the integration capabilities of three popular personal finance software options: Mint, Personal Capital, and YNAB (You Need A Budget). Note that integration capabilities can change over time, so it’s always best to check the software provider’s website for the most up-to-date information.

| Software | Bank Account Integration | Credit Card Integration | Investment Platform Integration |

|---|---|---|---|

| Mint | Excellent; supports a wide range of banks and credit unions | Excellent; supports major credit card issuers | Good; integrates with many popular brokerage accounts |

| Personal Capital | Excellent; supports a wide range of banks and credit unions | Excellent; supports major credit card issuers | Excellent; comprehensive integration with various investment platforms, including detailed portfolio analysis |

| YNAB | Good; supports many banks and credit unions, but may require manual connection in some cases | Good; supports major credit card issuers | Limited; primarily focuses on budgeting and does not offer extensive investment tracking |

Examples of Enhanced User Experience Through Integration

Effective integration significantly enhances the user experience. For example, automatically categorizing transactions from bank and credit card statements saves users from manually tagging each expense, providing a more efficient and less time-consuming budgeting process. Similarly, the ability to view all financial accounts – checking, savings, credit cards, and investments – in a single dashboard offers a comprehensive overview of one’s financial health, simplifying financial planning and decision-making.

The automated aggregation of investment data allows users to easily monitor their portfolio performance, track asset allocation, and make informed investment decisions without logging into multiple platforms. Imagine effortlessly tracking your net worth across all your accounts in real-time, or automatically generating insightful reports based on your spending habits; these are all benefits facilitated by seamless integration.

Personal Finance

Effective personal finance management is crucial for achieving long-term financial well-being. Understanding fundamental financial principles and employing sound strategies are essential for building wealth, securing financial stability, and achieving personal financial goals. This section explores the broader context of personal finance, encompassing financial literacy, budgeting approaches, best practices for saving and investing, and debt management.

Financial Literacy and Effective Personal Finance Management

Financial literacy plays a pivotal role in successful personal finance management. A strong understanding of concepts like budgeting, saving, investing, and debt management empowers individuals to make informed financial decisions, avoid costly mistakes, and achieve their financial aspirations. Without financial literacy, individuals may struggle to navigate the complexities of personal finance, potentially leading to financial instability and missed opportunities.

For example, a lack of understanding regarding compound interest could significantly hinder long-term investment growth.

Budgeting Approaches

Several budgeting methods can help individuals track their income and expenses. Two popular approaches are the 50/30/20 rule and zero-based budgeting. The 50/30/20 rule suggests allocating 50% of after-tax income to needs (housing, food, transportation), 30% to wants (entertainment, dining out), and 20% to savings and debt repayment. Zero-based budgeting, on the other hand, involves assigning every dollar of income to a specific expense category, ensuring all spending is accounted for and preventing overspending.

Choosing the right budgeting method depends on individual financial goals and preferences.

Best Practices for Saving, Investing, and Debt Management

Effective saving, investing, and debt management are interconnected aspects of sound personal finance. Saving involves setting aside a portion of income regularly to build an emergency fund and achieve long-term financial goals. Investing involves allocating funds into assets with the potential for growth, such as stocks, bonds, or real estate. A diversified investment portfolio can help mitigate risk and maximize returns.

Debt management focuses on strategically reducing and eliminating debt through methods like debt consolidation or the debt snowball/avalanche methods. For instance, prioritizing high-interest debt repayment through the debt avalanche method can save money on interest payments in the long run.

Creating a Comprehensive Personal Financial Plan

A well-structured personal financial plan is essential for achieving long-term financial success. The following flowchart illustrates the key steps involved:

Future Trends in Personal Finance Software

The landscape of personal finance software is rapidly evolving, driven by advancements in technology and shifting consumer expectations. We are moving beyond basic budgeting and tracking tools towards highly personalized, intelligent systems that proactively manage our financial well-being. This evolution is fueled by several key trends, significantly impacting how individuals interact with their finances.

The Role of Artificial Intelligence and Machine Learning

AI and machine learning are revolutionizing personal finance software. These technologies enable sophisticated features like predictive analytics, identifying potential spending risks or investment opportunities based on user spending patterns and market trends. For instance, AI can analyze transaction data to automatically categorize expenses, flag unusual activity, and even suggest ways to reduce spending in specific areas. Machine learning algorithms can also personalize investment portfolios based on risk tolerance and financial goals, offering more tailored advice than traditional methods.

This level of automation simplifies financial management and empowers users to make more informed decisions.

Personalized Financial Advice and Robo-Advisors

The increasing availability of personalized financial advice delivered through software is a significant trend. Robo-advisors, automated investment platforms using algorithms to manage portfolios, are becoming increasingly popular, offering low-cost investment solutions previously inaccessible to many. These platforms leverage AI and machine learning to provide customized investment strategies based on individual risk profiles and financial goals. Beyond investments, personalized financial advice extends to budgeting, debt management, and retirement planning, offering tailored strategies and actionable insights.

For example, a robo-advisor might suggest adjusting a user’s investment allocation based on their approaching retirement age or recommend a debt repayment strategy tailored to their income and debt levels.

The Impact of Open Banking on Personal Finance Software Development

Open banking, which allows consumers to securely share their financial data with third-party providers, is transforming personal finance software. This increased data accessibility enables the development of more comprehensive and integrated financial management tools. Open banking allows personal finance apps to connect to multiple bank accounts, credit cards, and investment accounts, providing a holistic view of a user’s financial situation.

This aggregated data can be used to generate more accurate financial reports, provide more precise budgeting tools, and offer more effective personalized financial advice. For example, an app could use open banking data to automatically reconcile accounts, track net worth, and identify potential areas for financial improvement across all connected accounts.

Predicted Evolution of Personal Finance Software in the Next 5 Years

The predicted evolution of personal finance software over the next five years can be visualized as a dynamic, interconnected ecosystem. Imagine a central hub, representing the personal finance software application, connected to various external services through secure APIs. These connections represent open banking integration with various financial institutions. Around the central hub, smaller, interconnected circles represent various features, such as AI-powered budgeting tools, personalized investment recommendations from robo-advisors, and automated debt management strategies.

The size of these circles will increase over time, representing the growing sophistication and integration of these features. The overall image would show a significant increase in connectivity and automation, with the central hub becoming more intelligent and proactive in managing users’ finances. The color scheme could use vibrant blues and greens to convey a sense of growth and stability, while the lines connecting the circles would be bright, showcasing the seamless data flow enabled by open banking.

The overall design should be clean and modern, reflecting the technological advancements driving the evolution of personal finance software. The central hub would progressively become more intelligent, with the AI and machine learning capabilities represented by a glowing core, symbolizing its growing analytical power and predictive capabilities.

Ultimately, choosing the right personal finance software depends on individual needs and financial goals. By understanding the core functionalities, comparing available options, and prioritizing data security, individuals can effectively leverage technology to enhance their financial well-being. Embracing financial literacy and staying informed about emerging trends will further contribute to long-term financial success. The journey towards financial mastery begins with informed choices and a commitment to proactive management.

Essential Questionnaire

What is the best personal finance software for beginners?

Mint and Personal Capital are often recommended for beginners due to their user-friendly interfaces and comprehensive features.

Is my data safe with personal finance software?

Reputable software providers employ robust security measures, including encryption and multi-factor authentication. However, it’s crucial to research a provider’s security practices before sharing sensitive financial information.

Can I use personal finance software if I don’t have a lot of technical skills?

Many personal finance software options are designed with intuitive interfaces, requiring minimal technical expertise. Start with a free trial or a basic plan to familiarize yourself with the software before committing to a paid subscription.

How much does personal finance software typically cost?

Pricing models vary widely, ranging from free options with limited features to premium subscriptions offering advanced functionalities. Many providers offer free trials or freemium models, allowing you to test the software before committing to a paid version.