Mastering personal finance can feel daunting, but creating a budget is the cornerstone of financial well-being. This guide provides a practical, step-by-step approach to building a budget tailored to your individual needs and financial goals, empowering you to take control of your financial future. We’ll explore various budgeting methods, debt management strategies, and saving and investing techniques to help you achieve financial stability and security.

From defining your short-term and long-term financial aspirations to tracking your income and expenses meticulously, we’ll navigate the process of creating a realistic and sustainable budget. We’ll also delve into crucial aspects like understanding different budgeting methodologies, managing debt effectively, and planning for your future through saving and investing. This comprehensive guide aims to equip you with the knowledge and tools necessary to confidently manage your finances.

Tracking Your Income and Expenses

Accurately tracking your income and expenses is the cornerstone of effective budgeting. Without a clear understanding of where your money comes from and where it goes, creating a realistic and achievable budget is nearly impossible. This section will explore various methods for tracking your finances and highlight some often-overlooked expenses.

Methods for Tracking Income and Expenses

Choosing the right method for tracking your finances depends on your personal preferences and technological comfort level. Each approach offers unique advantages and disadvantages. Consider your needs carefully before making a selection.

| Method | Ease of Use | Features | Cost |

|---|---|---|---|

| Spreadsheet (e.g., Microsoft Excel, Google Sheets) | Moderate. Requires some familiarity with spreadsheet software. | Highly customizable; allows for complex calculations and visualizations; readily accessible offline. | Free (if using open-source options); subscription cost for premium features in some cases. |

| Budgeting App (e.g., Mint, YNAB, Personal Capital) | Generally easy; user-friendly interfaces. | Automated transaction tracking (often requires linking bank accounts); expense categorization; budgeting tools; reporting features; some offer financial advice. | Free (often with limited features); subscription for premium features. |

| Notebook and Pen | Simple; requires minimal technological skills. | Completely offline; provides a tangible record of your finances. | Low cost (only the price of a notebook and pen). |

Commonly Overlooked Expenses

Many hidden expenses can significantly impact your budget if not accounted for. Being aware of these potential drainers on your finances is crucial for accurate budget planning.

- Subscription Services: Streaming services, gym memberships, software subscriptions, and other recurring charges can quickly add up. Regularly review your subscriptions and cancel any you no longer use.

- Small Purchases: Daily expenses like coffee, snacks, and impulse buys can accumulate into substantial sums over time. Tracking these small purchases can reveal areas where you can easily cut back.

- Unplanned Car Expenses: Unexpected repairs, maintenance, or fuel price fluctuations can disrupt your budget. Setting aside a dedicated fund for car-related expenses can help mitigate the impact of unforeseen costs. For example, setting aside $100 a month for car maintenance may prevent a $500 repair from becoming a financial emergency.

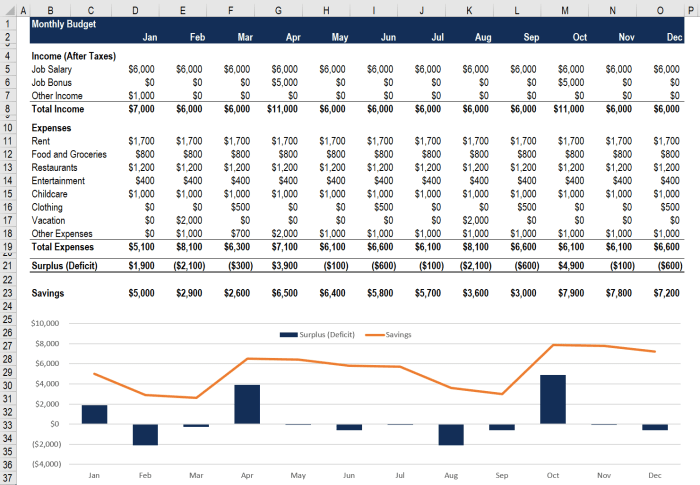

Sample Monthly Income and Expense Tracking Sheet

This sample sheet provides a basic framework for tracking your income and expenses. You can adapt it to suit your specific needs.

- Income:

- Salary: $XXXX

- Side Hustle Income: $XXX

- Other Income (e.g., Interest): $XX

- Total Income: $XXXX

- Expenses:

- Housing (Rent/Mortgage): $XXX

- Utilities (Electricity, Water, Gas): $XXX

- Transportation (Car Payment, Gas, Public Transport): $XXX

- Groceries: $XXX

- Dining Out: $XXX

- Entertainment: $XXX

- Clothing: $XXX

- Personal Care: $XX

- Debt Payments: $XXX

- Savings: $XXX

- Other Expenses: $XXX

- Total Expenses: $XXXX

- Net Income (Income – Expenses): $XXX

Creating Your Budget

Now that you’ve tracked your income and expenses, it’s time to create a budget. A budget is a roadmap for your money, helping you allocate funds to achieve your financial goals. This section will explore different budgeting methods and strategies to help you find the best fit for your financial situation.

The 50/30/20 Budgeting Rule

The 50/30/20 rule is a simple yet effective budgeting guideline. It suggests allocating your after-tax income as follows: 50% for needs, 30% for wants, and 20% for savings and debt repayment.Needs encompass essential expenses like housing, groceries, transportation, and utilities. Wants include discretionary spending such as entertainment, dining out, and hobbies. Savings and debt repayment prioritize your financial future and reducing debt.Let’s illustrate with an example: Suppose your monthly after-tax income is $3,

000. Following the 50/30/20 rule

* Needs (50%): $1,500 (Rent: $1000, Groceries: $300, Transportation: $200)

Wants (30%)

$900 (Dining out: $300, Entertainment: $300, Hobbies: $300)

Savings & Debt Repayment (20%)

$600 (Savings: $400, Debt Payment: $200)This is just an example, and the allocation will vary depending on individual circumstances. The key is to consciously categorize your spending and allocate your income accordingly.

Zero-Based Budgeting vs. Envelope System

Two popular budgeting methods are zero-based budgeting and the envelope system. Both aim to track every dollar, but their approaches differ.

| Method | Pros | Cons | Suitability |

|---|---|---|---|

| Zero-Based Budgeting | Provides a clear picture of your finances; helps prioritize spending; allows for mindful allocation of every dollar. | Requires significant upfront time and effort; can be rigid and inflexible; requires meticulous tracking. | Individuals who are highly organized and detail-oriented; those aiming for specific financial goals. |

| Envelope System | Simple and visual; promotes mindful spending; helps avoid overspending in specific categories. | Requires physical cash; less flexible; can be inconvenient for online transactions. | Individuals who prefer a hands-on approach; those who struggle with impulse spending; suitable for beginners. |

Categorizing Expenses

Categorizing expenses is crucial for understanding your spending habits and making informed budgeting decisions. By grouping similar expenses, you can identify areas where you might be overspending and adjust your budget accordingly. This allows for better financial control and informed decision-making.Here are five example expense categories:

- Housing (Rent/Mortgage, Property Taxes, Home Insurance)

- Transportation (Car Payment, Gas, Public Transportation, Maintenance)

- Groceries (Food, Household Supplies)

- Utilities (Electricity, Water, Gas, Internet)

- Entertainment (Dining Out, Movies, Concerts, Hobbies)

Creating a personal budget is not a one-time task but an ongoing process of planning, tracking, and adjusting. By consistently monitoring your spending, reviewing your financial goals, and adapting your budget as needed, you’ll cultivate healthy financial habits that pave the way for long-term financial success. Remember that seeking professional financial advice can provide invaluable support and guidance on your journey towards financial freedom.

Embrace the power of budgeting and embark on a path towards a more secure and prosperous future.

Answers to Common Questions

What if my income fluctuates?

Use an average monthly income over several months to create a baseline budget. Adjust your spending plan as needed based on your actual income each month.

How often should I review my budget?

Ideally, review and adjust your budget at least monthly, or more frequently if your financial situation changes significantly.

What if I can’t stick to my budget?

Identify areas of overspending, explore ways to cut back, and consider seeking professional financial advice to develop a more sustainable plan.

Are there any free budgeting apps available?

Yes, many free budgeting apps are available for both smartphones and computers. Research different options to find one that suits your needs and preferences.

Can I use a budgeting app alongside a spreadsheet?

Absolutely! Many people find it helpful to use both methods, using an app for quick tracking and a spreadsheet for more detailed analysis.