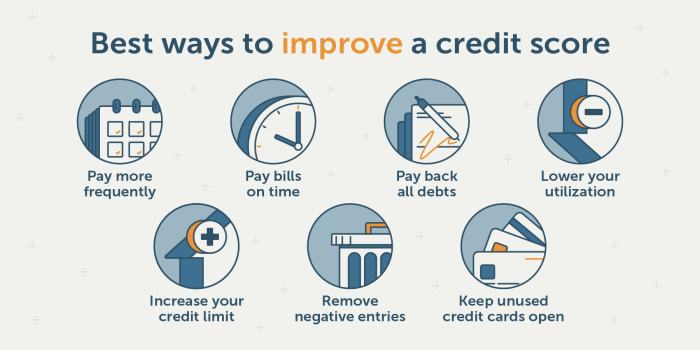

Navigating the world of credit scores can feel daunting, but understanding the key factors influencing your score empowers you to take control of your financial future. This guide provides a practical roadmap to improving your creditworthiness, covering everything from understanding the components of your score to developing effective strategies for managing debt and building a strong credit history. By following these steps, you can pave the way for better financial opportunities and a more secure future.

We will explore the five key factors that determine your credit score: payment history, amounts owed, length of credit history, new credit, and credit mix. Each factor plays a crucial role, and understanding their individual impact allows for targeted improvements. We’ll also delve into practical strategies for addressing common credit challenges, such as high credit utilization and late payments, and provide actionable advice for building a robust and healthy credit profile.

New Credit

Establishing and managing new credit accounts wisely is crucial for improving your credit score. The way you handle new credit applications significantly impacts your creditworthiness, affecting both the score itself and the interest rates you’ll receive on future loans. Understanding this process is key to building a strong credit profile.Applying for multiple credit accounts within a short period can negatively affect your credit score.

This is because each application results in a “hard inquiry,” which is a check of your credit report by a lender. Multiple hard inquiries within a short timeframe signal to lenders that you may be financially stressed or overextended, increasing their perceived risk. This increased risk translates to a lower credit score. The impact of multiple hard inquiries can vary depending on your existing credit history and the scoring model used, but generally, it’s best to minimize their occurrence.

Impact of Multiple Credit Applications

Each time you apply for credit, lenders perform a hard inquiry on your credit report. Too many hard inquiries within a short period (typically 12 months) can lower your credit score. Lenders see a flurry of applications as a potential sign of financial instability. For example, applying for five credit cards in one month will likely have a more negative impact than applying for one card every six months.

The impact isn’t permanent; the effect of hard inquiries typically diminishes over time, but it’s still a factor to consider when managing your credit. Credit scoring models weigh recent activity more heavily, so recent inquiries carry more weight than those from several years ago.

Strategies for Minimizing Credit Applications

Before applying for new credit, carefully consider your needs and existing financial situation. Avoid impulsive applications driven by attractive offers or marketing campaigns. Plan your credit applications strategically. If you need several new credit accounts, space out your applications over several months. Prioritize applications that are most important to your financial goals.

For instance, if you need a mortgage, focus on that application first and avoid applying for other credit lines while that process is underway. If you’re pre-approved for credit, this is a strong indicator of likelihood of approval and won’t create another hard inquiry on your credit report unless you formally accept the offer.

Benefits of Debt Consolidation

Debt consolidation involves combining multiple debts into a single loan. This can simplify your finances and potentially improve your credit score. A consolidated loan often comes with a lower interest rate than your existing debts, reducing your monthly payments and allowing you to pay off the debt faster. Furthermore, consolidating debt can reduce the number of accounts reported on your credit report, potentially improving your credit utilization ratio.

This is particularly helpful if you have many high-interest debt accounts. For example, someone with several high-interest credit cards could consolidate their debt into a personal loan with a lower interest rate. This can lead to a lower overall debt burden and improve their credit utilization ratio, ultimately contributing to a higher credit score. However, it’s important to note that the positive impact of debt consolidation on credit scores depends on responsible management of the consolidated loan.

Failing to make payments on the consolidated loan could have a severely negative impact on your credit.

Credit Mix

A diverse range of credit accounts can significantly impact your credit score. Lenders look favorably upon individuals who demonstrate responsible management across different types of credit, indicating a lower risk profile. Understanding the various credit types and their contribution to your overall credit health is crucial for improving your score.Your credit mix refers to the types of credit accounts you have.

A healthy credit mix generally includes a variety of credit products, demonstrating your ability to handle different financial responsibilities. This isn’t about the number of accounts, but rather the variety.

Types of Credit Accounts

Credit accounts fall into several main categories. Each type carries different levels of risk and responsibility for the lender, influencing how it impacts your credit score. A balanced mix helps showcase your financial maturity.

- Credit Cards: Revolving credit, where you can borrow up to a certain limit and pay it back over time, with interest charged on the outstanding balance. Responsible credit card use demonstrates your ability to manage debt effectively.

- Installment Loans: These loans have a fixed repayment schedule with a set number of payments over a specific period. Examples include auto loans, personal loans, and student loans. Successful repayment of these loans shows consistency in meeting financial obligations.

- Mortgages: A long-term loan secured by real estate. Responsible mortgage management is a strong indicator of financial stability and reliability.

Importance of a Diverse Credit Mix

A diverse credit mix shows lenders that you can successfully manage different types of credit accounts. It suggests a lower risk to lenders, potentially leading to better interest rates and increased approval chances for future credit applications. While not the sole determinant of your credit score, it is a contributing factor. For instance, someone with only credit cards might be perceived as higher risk than someone with a mix of credit cards, an auto loan, and a mortgage, assuming all accounts are managed responsibly.

Impact of a Single Credit Type versus a Diverse Mix

Having only one type of credit account, such as only credit cards, can limit your credit score potential. While responsible use of credit cards is important, a single type of account doesn’t fully showcase your ability to handle various financial responsibilities. Conversely, a diverse mix, showing responsible management across different credit types (credit cards, installment loans, mortgages), presents a more complete and favorable picture to lenders, potentially leading to a higher credit score.

This is because it demonstrates a wider range of financial experience and responsible behavior.

Monitoring Your Credit Report

Regularly reviewing your credit report is crucial for maintaining a healthy credit score. It allows you to identify and address any errors or fraudulent activity that could negatively impact your financial standing. By staying informed, you can proactively protect your credit and ensure accuracy in the information used to assess your creditworthiness.

Obtaining a Free Credit Report

You are entitled to a free credit report from each of the three major credit bureaus – Equifax, Experian, and TransUnion – once a year through AnnualCreditReport.com. This is the only official website authorized by law to provide these free reports. Avoid sites that claim to offer free reports but require payment or personal information beyond what’s needed for verification.

To obtain your report, you’ll need to provide your name, address, social security number, and date of birth. The process is straightforward and usually takes a few minutes to complete. After providing this information, you will be able to access your credit report from each of the three bureaus individually.

Disputing Inaccurate Information

If you discover any inaccuracies on your credit report, such as incorrect account information, late payments that weren’t yours, or accounts that don’t belong to you, you should immediately dispute them. Each credit bureau provides a process for filing a dispute. This typically involves submitting a dispute form, either online or by mail, outlining the specific inaccuracies and providing supporting documentation, such as proof of payment or a copy of a police report if fraud is suspected.

The credit bureau is then required to investigate the claim and update your report accordingly if the information is found to be incorrect. Keep records of all correspondence and documentation related to your dispute. It’s advisable to dispute errors with each bureau individually, as they may not share information with each other.

Credit Report Review Checklist

Before reviewing your report, gather any relevant financial documents, such as bank statements and loan agreements. This will help you verify the accuracy of the information presented. A thorough review should include checking for:

- Accuracy of personal information: Verify your name, address, social security number, and date of birth.

- Account accuracy: Check for any incorrect account numbers, balances, payment histories, or dates of opening and closing.

- Presence of fraudulent accounts: Look for accounts you did not open.

- Correct reporting of payment history: Ensure all payments are accurately reflected, noting any discrepancies.

- Inquiries: Review recent credit inquiries to identify any you don’t recognize.

- Public records: Verify the accuracy of any bankruptcies, judgments, or tax liens listed.

Following this checklist will help ensure a comprehensive review and allow you to identify any potential problems requiring further investigation or dispute. Remember to review your reports regularly to maintain a clear and accurate picture of your credit history.

Personal Finance Strategies

Improving your credit score isn’t solely about managing credit; it’s intrinsically linked to your overall financial health. A solid personal finance strategy forms the bedrock for a strong credit profile. By proactively managing your income and expenses, you can significantly reduce debt and improve your creditworthiness. This section will Artikel key strategies for building a robust financial foundation that supports better credit.

Effective personal finance management is crucial for improving your credit score. It allows you to gain control of your finances, enabling strategic debt reduction and building a financial safety net. This, in turn, positively impacts your credit report and score.

Budgeting for Debt Repayment and Savings

Creating a detailed budget is the cornerstone of responsible financial management. This involves meticulously tracking your income and expenses to understand your spending habits and identify areas for improvement. A well-structured budget should allocate funds towards essential expenses, debt repayment, and savings. Prioritizing debt repayment within your budget can accelerate the process of reducing your debt-to-income ratio, a key factor in credit score calculations.

For example, if your monthly income is $3000 and your expenses are $2000, you could allocate $500 towards debt repayment and $500 towards savings. This consistent allocation will contribute significantly to improving your credit health over time.

Building an Emergency Fund

An emergency fund acts as a financial safety net, protecting you from unexpected expenses that could otherwise lead to increased debt. Aim to save enough to cover 3-6 months of essential living expenses. This fund helps avoid the need to resort to high-interest credit cards or loans during emergencies, thereby preventing negative impacts on your credit score. For instance, if an unexpected car repair costs $1000, having an emergency fund eliminates the need to borrow money and potentially incur debt that could negatively affect your credit report.

This proactive approach ensures financial stability and safeguards your credit health.

The Relationship Between Saving and Credit Score Improvement

Saving money directly contributes to improving your credit score. Increased savings reduce your reliance on credit, lowering your debt-to-income ratio (DTI). A lower DTI demonstrates financial responsibility to lenders, leading to improved creditworthiness. For example, if you consistently save a portion of your income, you can use those savings to pay down high-interest debt like credit card balances.

This reduces your debt load and improves your credit utilization ratio, both of which positively influence your credit score. Furthermore, consistent savings show lenders your financial stability and responsible management of your finances.

Dispute Errors

Maintaining a healthy credit score requires vigilance. One crucial aspect often overlooked is proactively identifying and disputing inaccuracies on your credit reports. Errors on your report can significantly impact your creditworthiness, leading to higher interest rates and difficulty securing loans. Understanding the process of disputing these errors is essential for protecting your financial well-being.Errors on credit reports are surprisingly common.

These inaccuracies can range from simple data entry mistakes to more serious issues involving fraudulent accounts. Addressing these errors promptly is vital for preserving your credit score and preventing further complications. The process involves directly contacting the credit bureaus – Equifax, Experian, and TransUnion – and formally requesting a review of the disputed information.

The Process of Disputing Inaccurate Information

Disputing an error involves several steps. First, gather all relevant documentation supporting your claim. This might include bank statements, payment receipts, or copies of contracts. Next, you’ll need to submit a formal dispute letter to each credit bureau individually. These letters should clearly identify the inaccurate information, provide supporting evidence, and request its removal or correction.

Each bureau has its own dispute process, typically accessible through their website. You should expect a response within 30-45 days, though it can sometimes take longer. Crucially, retain copies of all correspondence with the credit bureaus.

Examples of Common Credit Report Errors

Common errors include incorrect account information, such as the wrong account number, balance, or payment history. Another frequent issue is accounts that don’t belong to you – accounts opened fraudulently in your name. Delinquent accounts that were paid on time can also appear erroneously. Incorrect personal information, like your address or Social Security number, is another possibility.

Finally, bankruptcies or judgments that have been legally discharged might still appear on your report.

Documenting Communication with Credit Bureaus

Meticulous record-keeping is crucial throughout the dispute process. Keep copies of all letters you send, including any supporting documents. Note the date you sent each letter and the method of delivery (mail, email, fax). Similarly, record the date and method of any responses received from the credit bureaus. This detailed documentation will be invaluable if you need to escalate your dispute or demonstrate your efforts to correct the inaccuracies.

Consider using a spreadsheet or a dedicated file to organize all your communications. This systematic approach helps ensure that no detail is overlooked, strengthening your case and streamlining the dispute resolution process.

Improving your credit score is a journey, not a race. Consistent effort and mindful financial habits are key to achieving long-term credit health. By diligently monitoring your credit report, proactively managing your debt, and making informed financial decisions, you can significantly enhance your creditworthiness and unlock a wider range of financial opportunities. Remember, building a strong credit score is a testament to responsible financial management and opens doors to lower interest rates, better loan terms, and a more secure financial future.

Take charge of your credit today and reap the rewards tomorrow.

Query Resolution

What is a good credit score?

Generally, a credit score above 700 is considered good, while scores above 800 are excellent. However, the specific thresholds vary depending on the scoring model used.

How often should I check my credit report?

You are entitled to a free credit report from each of the three major credit bureaus (Equifax, Experian, and TransUnion) annually through AnnualCreditReport.com. Checking regularly helps you identify and address any errors or fraudulent activity.

Can I improve my credit score quickly?

While significant improvements take time, consistent positive actions like paying bills on time and reducing debt can yield noticeable results within a few months. The speed of improvement depends on your starting point and the actions you take.

What if I have a bankruptcy on my credit report?

Bankruptcy remains on your credit report for 7-10 years, but its negative impact diminishes over time. Focus on establishing positive credit habits after bankruptcy to rebuild your score.