Navigating the complexities of debt can feel overwhelming, but reclaiming financial control is entirely achievable. This guide explores effective debt reduction strategies, from budgeting techniques and negotiation tactics to consolidation options and the psychological aspects of debt management. We’ll delve into proven methods to help you regain financial stability and build a brighter future.

Understanding your debt landscape is the first step. We’ll compare popular approaches like the snowball and avalanche methods, examining their pros and cons to help you choose the best strategy for your unique circumstances. Beyond the mechanics of repayment, we’ll also address the emotional challenges often associated with debt, offering practical coping mechanisms and motivational strategies to keep you on track.

Understanding Debt Reduction Strategies

Tackling significant debt can feel overwhelming, but employing a strategic approach can significantly improve your financial outlook. Understanding different debt reduction strategies and their implications is crucial for choosing the most effective method for your specific circumstances. This section will explore two popular methods—the snowball and avalanche methods—and compare them to other debt reduction strategies.

The Snowball Method of Debt Reduction

The snowball method prioritizes paying off the smallest debts first, regardless of interest rates. This approach focuses on building momentum and psychological wins, motivating you to continue the debt reduction process. The feeling of accomplishment from quickly eliminating smaller debts can encourage persistence when tackling larger, more challenging debts.

- List your debts: Create a list of all your debts, including the creditor, balance, and interest rate.

- Order debts smallest to largest: Arrange your debts from smallest balance to largest, irrespective of interest rates.

- Make minimum payments on all debts except the smallest: Ensure you meet the minimum payment requirements for all your debts, except the smallest one.

- Allocate extra funds to the smallest debt: Direct any extra money you can afford towards paying off the smallest debt as quickly as possible.

- Repeat the process: Once the smallest debt is paid off, roll that payment amount into the next smallest debt, continuing this snowball effect until all debts are eliminated.

The Avalanche Method of Debt Reduction

The avalanche method prioritizes paying off debts with the highest interest rates first, regardless of the balance. This approach minimizes the total interest paid over time, leading to potential long-term savings. While the initial progress might seem slower than the snowball method, the financial benefits are often more significant in the long run.

- List your debts: Create a list of all your debts, including the creditor, balance, and interest rate.

- Order debts by interest rate: Arrange your debts from highest interest rate to lowest.

- Make minimum payments on all debts except the highest interest rate debt: Ensure you meet the minimum payment requirements for all debts except the one with the highest interest rate.

- Allocate extra funds to the highest interest rate debt: Direct any extra money you can afford towards paying off the debt with the highest interest rate as quickly as possible.

- Repeat the process: Once the highest interest rate debt is paid off, roll that payment amount into the next highest interest rate debt, continuing until all debts are eliminated.

Comparison of Debt Reduction Strategies

The snowball and avalanche methods are just two approaches. Other strategies, such as debt consolidation, balance transfers, and debt management plans, offer different advantages and disadvantages.

| Strategy | Pros | Cons | Best For |

|---|---|---|---|

| Snowball Method | Motivational, quick wins | May cost more in interest overall | Individuals needing psychological encouragement |

| Avalanche Method | Saves money on interest in the long run | Can be demotivating initially | Individuals prioritizing minimizing total interest paid |

| Debt Consolidation | Simplifies payments, potentially lower interest rate | May require good credit, potential for higher fees | Individuals with multiple debts and good credit |

| Balance Transfers | Low or 0% introductory APR | Balance transfer fees, interest rate increase after introductory period | Individuals with good credit seeking short-term interest savings |

| Debt Management Plan (DMP) | Lower monthly payments, professional guidance | Impacts credit score, fees may apply | Individuals struggling to manage multiple debts |

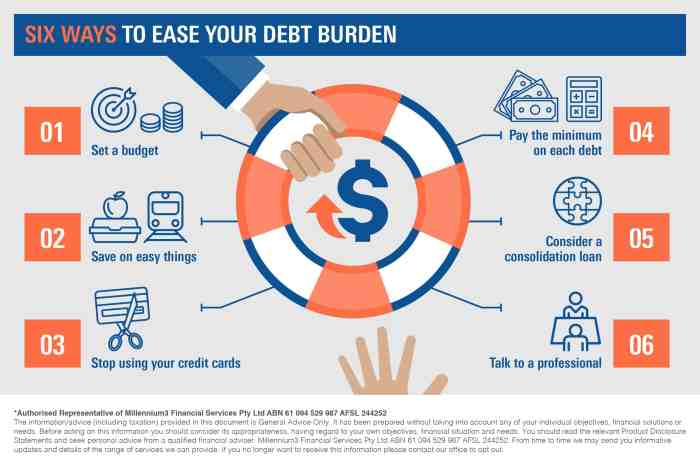

Budgeting and Debt Management

Effective budgeting and debt management are crucial for successfully reducing debt and improving your financial well-being. A well-structured budget allows you to allocate your income strategically, prioritizing debt repayment while still covering essential living expenses. This process requires careful tracking of expenses, identifying areas for savings, and building a financial safety net.

Creating a realistic budget involves carefully assessing your income and expenses. This process helps you understand where your money is going and allows you to make informed decisions about how to allocate your funds to maximize debt repayment while maintaining a comfortable standard of living. Careful planning is key to ensuring both your short-term and long-term financial health.

Sample Budget Template

A sample budget template can help you visualize your income and expenses. The following template demonstrates a practical approach to allocating funds for debt repayment while maintaining essential expenses. Remember to tailor this template to your specific income and expenses.

- Income: List all sources of income (e.g., salary, part-time job, investments).

- Essential Expenses: Housing (rent/mortgage), utilities (electricity, water, gas), groceries, transportation, healthcare insurance, minimum debt payments (credit cards, loans).

- Debt Repayment: Allocate a significant portion of your income towards debt repayment. Prioritize high-interest debts first (e.g., credit cards). Consider debt avalanche or debt snowball methods.

- Non-Essential Expenses: Entertainment, dining out, subscriptions, shopping. These are areas where you can often find savings.

- Savings: Include a line item for savings, aiming for at least 10-20% of your income. This includes building an emergency fund.

- Other Expenses: Include any other regular expenses (e.g., childcare, pet care).

Expense Tracking and Savings Identification

Effectively tracking expenses is vital for identifying areas where you can cut back and accelerate debt reduction. Several methods exist to help you monitor your spending habits and pinpoint unnecessary expenses.

- Use budgeting apps: Many apps automatically categorize your transactions, providing a clear picture of your spending habits.

- Maintain a spreadsheet: Manually recording your expenses allows for detailed analysis and helps you identify trends.

- Review bank and credit card statements: Regularly review your statements to identify recurring expenses and areas for potential savings.

- Identify recurring subscriptions: Cancel any unused or unnecessary subscriptions (e.g., streaming services, gym memberships).

- Reduce dining out and entertainment expenses: Cook at home more often and explore free or low-cost entertainment options.

Emergency Fund Importance

An emergency fund acts as a crucial safety net, preventing further debt accumulation during unexpected financial setbacks. Having readily available funds reduces the need to borrow money during emergencies, such as job loss, medical expenses, or car repairs.

- Aim for 3-6 months of living expenses: This provides a cushion during unforeseen circumstances.

- Prioritize building the emergency fund before aggressively paying down debt: A small emergency fund can prevent a larger debt problem.

- Keep the emergency fund in a readily accessible account: A high-yield savings account or money market account is ideal.

- Automate savings: Set up automatic transfers from your checking account to your savings account.

Negotiating with Creditors

Negotiating with creditors can be a crucial step in effectively managing and reducing debt. A proactive approach, coupled with a clear understanding of your financial situation, can significantly improve your chances of reaching a favorable agreement. Remember, the goal is to find a solution that works for both you and your creditors.Successfully negotiating with creditors involves a strategic approach that combines preparation, communication, and persistence.

This process allows individuals to potentially lower their monthly payments, reduce interest rates, and even consolidate multiple debts into a single, more manageable payment. While it requires effort and patience, the potential benefits are substantial in alleviating financial stress and accelerating debt repayment.

Lowering Interest Rates

Lowering your interest rate can dramatically reduce the total amount you pay over the life of your loan. Before contacting your creditor, gather all relevant documentation, including your credit report and account statements. This demonstrates your preparedness and seriousness. When contacting the creditor, be polite, respectful, and clearly explain your financial situation. Highlight your consistent payment history, if applicable, and emphasize your commitment to paying off your debt.

Propose a specific, realistic lower interest rate, ideally backed by research into current market rates for similar loans. Be prepared to negotiate, but also have a walk-away point in mind. For example, if you currently have a credit card with a 20% interest rate and you’ve consistently made on-time payments for the last year, you might propose a reduction to 15%, presenting evidence of your responsible financial behavior.

Establishing Payment Plans

Setting up a payment plan with creditors provides a structured approach to debt repayment, preventing delinquency and potential damage to your credit score. Contact each creditor individually to discuss your financial difficulties and propose a payment plan that aligns with your budget. Be clear about the amount you can realistically afford to pay each month. A well-defined payment plan typically includes the total amount owed, the proposed monthly payment, and the repayment timeframe.

Consider offering a lump-sum payment, if possible, to demonstrate your good faith and potentially secure a more favorable agreement. For instance, if you owe $5,000 on a credit card and can afford $100 per month, you could propose a payment plan of $100 per month for 50 months, along with a potential one-time payment of $500 at the start.

Always get the agreement in writing to avoid future misunderstandings.

Challenges and Solutions

Negotiating with creditors can present several challenges. Creditors may be unwilling to negotiate, especially if you have a history of missed payments. In such cases, consider seeking professional help from a credit counselor who can mediate the negotiation process. Another challenge might be the creditor’s inflexible policies or lack of responsiveness. If you encounter difficulty getting a response, try contacting the creditor through different channels, such as phone, email, and mail.

Persistence is key; don’t be discouraged by initial setbacks. Finally, be prepared for the possibility of rejection. If your initial proposal is rejected, be prepared to counter with a revised offer or explore alternative debt management strategies.

Debt Consolidation and Refinancing

Debt consolidation and refinancing are powerful tools in your debt reduction arsenal, offering the potential to simplify your finances and save money. Understanding how these strategies work and when they are most appropriate is crucial for effectively managing your debt. This section will explore the processes involved, their advantages and disadvantages, and provide a comparison of common options.Debt consolidation involves combining multiple debts into a single payment.

This streamlines your finances, potentially lowering your monthly payments and simplifying the repayment process. Refinancing, on the other hand, focuses on replacing an existing loan with a new one, often with better terms, such as a lower interest rate. Both strategies can significantly impact your debt repayment journey.

Debt Consolidation Process and Beneficial Situations

Debt consolidation typically involves securing a new loan (such as a personal loan or home equity loan) or using a balance transfer credit card to pay off existing debts. Once the new loan is secured, the lender pays off your existing creditors, leaving you with a single monthly payment. This process is most beneficial when you have high-interest debts, multiple creditors, or are struggling to manage multiple payments.

For example, someone with several credit cards carrying high interest rates could consolidate them into a lower-interest personal loan, making repayment more manageable. Similarly, individuals with medical debt or high-interest store credit cards might find consolidation advantageous.

Benefits and Drawbacks of Refinancing High-Interest Debt

Refinancing high-interest debt offers the potential for substantial savings. By securing a loan with a lower interest rate, you reduce the total amount of interest paid over the life of the loan, leading to faster debt repayment. However, refinancing isn’t always the best option. Drawbacks include potential closing costs associated with the new loan, the possibility of extending the repayment period (leading to more interest paid overall despite a lower rate), and the risk of impacting your credit score if a hard credit inquiry is performed.

For instance, a person with a car loan at 18% APR might significantly benefit from refinancing to a lower rate, even if it extends the loan term slightly. However, if the closing costs are high, the savings might be offset.

Comparison of Debt Consolidation Options

Choosing the right debt consolidation option depends on your individual financial circumstances and creditworthiness. Below is a comparison of two common methods:

| Feature | Personal Loan | Balance Transfer Credit Card |

|---|---|---|

| Interest Rate | Typically fixed, often lower than credit card interest rates. | Often 0% for a promotional period, then a variable rate that can be high. |

| Fees | Origination fees may apply. | Balance transfer fees and potential penalty fees for late payments. |

| Repayment Period | Fixed repayment schedule over a set term (e.g., 36 or 60 months). | Minimum monthly payments are required, but you can pay more to pay it off faster. |

| Credit Score Impact | A hard credit inquiry can temporarily lower your credit score. | A hard credit inquiry can temporarily lower your credit score. Managing the balance carefully is crucial to maintain a good credit score. |

Personal Finance and Debt Reduction

Effective debt reduction isn’t just about paying down balances; it’s intrinsically linked to a well-structured personal financial plan. A comprehensive plan provides the framework for prioritizing debt repayment, managing expenses, and building a secure financial future. Ignoring personal finance principles while tackling debt often leads to unsustainable strategies and ultimately, failure to achieve financial freedom.Personal financial planning offers a roadmap for strategically addressing debt.

By integrating debt reduction goals into a broader financial strategy, individuals gain a clearer picture of their overall financial health and can make informed decisions about resource allocation. This holistic approach ensures that debt repayment doesn’t come at the expense of other crucial financial goals, such as saving for retirement or emergencies.

Integrating Debt Reduction Goals into a Financial Plan

A successful personal financial plan incorporates specific, measurable, achievable, relevant, and time-bound (SMART) debt reduction goals. This involves analyzing current income and expenses, identifying areas for savings, and determining a realistic repayment schedule for each debt. For instance, someone with multiple debts might prioritize paying off high-interest debts first using the avalanche method, while simultaneously building an emergency fund to prevent future debt accumulation.

The plan should also include strategies for avoiding future debt, such as creating a realistic budget and sticking to it. Regular review and adjustments are crucial to adapt to changing circumstances and maintain progress.

Utilizing Resources and Tools for Financial Planning and Debt Management

Several resources and tools can significantly aid in both personal financial planning and debt management. Budgeting apps, such as Mint or YNAB (You Need A Budget), provide automated tracking of income and expenses, offering insights into spending habits and identifying areas for potential savings. Debt repayment calculators, readily available online, help individuals determine the time it will take to pay off debts under various scenarios, assisting with strategy selection.

Furthermore, free online courses and workshops offered by organizations like the National Foundation for Credit Counseling (NFCC) provide valuable education on budgeting, debt management, and financial planning. These resources empower individuals to take control of their finances and make informed decisions about their debt. Finally, seeking guidance from a certified financial planner can offer personalized advice and support in navigating complex financial situations.

The Psychology of Debt and Motivation

Managing debt effectively involves not only financial strategies but also a deep understanding of the psychological factors at play. The emotional toll of debt can be significant, hindering progress and exacerbating financial stress. Addressing these emotional challenges is crucial for successful debt reduction.The emotional landscape of debt is often characterized by feelings of guilt, shame, anxiety, and even hopelessness.

These emotions can lead to avoidance behaviors, making it difficult to confront the problem head-on. This cycle of avoidance and negative emotions can be self-perpetuating, making debt reduction feel overwhelming and unattainable. Understanding these emotional responses is the first step towards developing effective coping mechanisms.

Emotional Challenges and Coping Strategies

Developing effective coping mechanisms is vital for navigating the emotional challenges associated with debt management. These strategies can help individuals manage stress, build resilience, and maintain motivation throughout the debt reduction process.

For example, feelings of guilt and shame are common. Individuals might blame themselves for their financial situation, leading to self-criticism and inaction. A helpful coping strategy involves reframing negative self-talk. Instead of focusing on past mistakes, concentrate on the positive steps being taken towards financial recovery. Practicing self-compassion and acknowledging that financial difficulties can affect anyone is also crucial.

Anxiety and stress are often associated with the weight of debt. Techniques like mindfulness meditation, deep breathing exercises, and regular physical activity can help manage these feelings. Seeking support from a therapist or counselor can also provide valuable tools and strategies for managing stress and anxiety.

Hopelessness can arise when debt seems insurmountable. Breaking down the debt reduction journey into smaller, manageable goals can combat this feeling. Focusing on progress, no matter how small, can build momentum and maintain motivation. Celebrating milestones along the way, such as paying off a specific credit card or reaching a debt reduction target, reinforces positive behavior and provides a sense of accomplishment.

Setting Realistic Goals and Celebrating Milestones

Setting realistic, achievable goals is paramount for maintaining motivation and avoiding discouragement. Unrealistic expectations can lead to feelings of failure and contribute to a sense of hopelessness. Therefore, it is essential to establish a debt reduction plan that aligns with an individual’s financial capabilities and lifestyle.

Begin by creating a comprehensive budget to track income and expenses accurately. This will provide a clear picture of your financial situation and help you identify areas where you can cut back on spending. Once you have a realistic understanding of your financial resources, you can set attainable goals, such as paying off the smallest debt first or allocating a specific amount towards debt repayment each month.

Regularly reviewing and adjusting your goals as needed ensures that your plan remains adaptable and effective.

Celebrating milestones along the way is crucial for maintaining momentum and positive reinforcement. Acknowledge and reward yourself for reaching significant benchmarks, such as paying off a credit card or reducing your overall debt by a certain percentage. These celebrations, whether large or small, serve as powerful reminders of your progress and motivate you to continue working towards your debt-free goal.

These celebrations can be simple – a nice meal, a movie night, or anything that brings you joy without adding to your debt.

Motivational Infographic: The Long-Term Benefits of Becoming Debt-Free

The infographic depicts a vibrant, upward-trending graph symbolizing financial freedom. The graph’s upward trajectory is emphasized with a bright, positive color, contrasting sharply with the dull, muted colors representing debt. At the base of the graph, a person is shown burdened down by a heavy chain representing debt, their face expressing stress and worry. As the graph ascends, the chain gradually loosens and finally breaks free, and the person’s expression transforms into one of relief and happiness.

The image further displays several key benefits of being debt-free: a picture of a comfortable home representing increased financial security; a happy family enjoying a vacation, representing improved lifestyle and opportunities; and a smiling individual confidently pursuing their career goals, symbolizing reduced stress and enhanced career prospects. Finally, a large, clear font proclaims “Debt-Free: Your Path to Financial Freedom” across the top of the infographic.

The overall visual tone is one of optimism, hope, and the promise of a brighter future.

Taking control of your debt is a journey, not a sprint. By implementing a well-defined plan, incorporating smart budgeting practices, and actively engaging with your creditors, you can significantly reduce your debt burden and pave the way for a more secure financial future. Remember that seeking professional financial advice when needed can provide invaluable support and guidance throughout this process.

The path to financial freedom begins with informed action and consistent effort.

Expert Answers

What is the difference between debt consolidation and debt refinancing?

Debt consolidation combines multiple debts into a single payment, often at a lower interest rate. Refinancing involves replacing an existing loan with a new one, typically with better terms.

Can I negotiate with creditors even if I’m not behind on payments?

Yes, you can often negotiate lower interest rates or payment plans even if you’re current on your payments. Demonstrating a commitment to repayment strengthens your negotiating position.

What if I can’t afford my minimum payments?

Contact your creditors immediately to discuss options like hardship programs or payment plans. Ignoring the issue will only worsen the situation.

How long does it typically take to pay off debt?

The timeframe depends on the amount of debt, interest rates, and your repayment plan. Consistency and a realistic budget are key factors.